- Collide - Generational Leadership

- Posts

- The Real Reason Millennials Kept Asking for Raises

The Real Reason Millennials Kept Asking for Raises

Why ‘entitlement’ isn’t the problem—it’s inherited expenses, bottom-up budgeting, and a generation leaders still misunderstand.

Ryan Vet

July 15, 2025

“I need a raise!” The familiar refrain that many managers faced as Millennials entered their workplace. But this constant pursuit of higher-paying gigs was not limited to Millennials, the pattern has continued with Gen Z and is certain to persist beyond.

A unique phenomenon occurred with the Millennial generation when it came to personal finance. Such major shifts in personal budgeting had only occurred fractionally and slowly with previous generations: the Silent Generation, with the advent of personal automobiles, along with the availability of the 30-year mortgage.

Millennials inherited a perfect storm whipping their personal finances into turmoil. It happened rapidly. It happened quietly. And to this day, many leaders, and even Millennials are failing to see how these moves redefined budgeting.

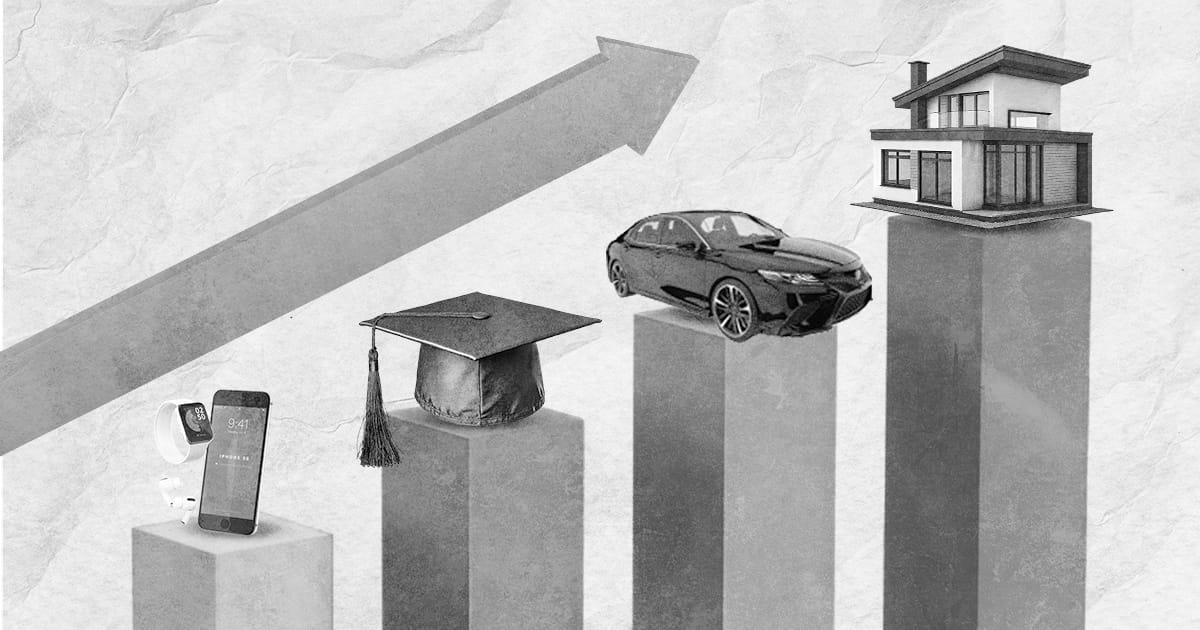

Millennials didn’t decide to redefine personal finance, they inherited a budget baseline so inflated that they built their budgets from the ground up. No longer “income first, spending second.” Subconsciously, they adapted a bottom-up budgeting model: account for “essential” costs before you know what you can afford.

The New “Essentials”

Once upon a simpler time, a cell phone was a luxury. For Millennials, it became a lifeline. By the late 1990s and early 2000s, nearly every teen from high school to college had a mobile phone and constant internet access. These were no longer extras; they were prerequisites for friends, work, learning, even survival (Pew, 2019).

It didn’t stop with connectivity. Today’s “monthly must-haves” are subscriptions: streaming, gaming, fitness, food, and productivity. The typical American now carries an average of 8.4 subscriptions costing about $118–$237 monthly, with nearly 40% of Millennials relying entirely on these recurring services for daily essentials (Savanta, 2024; Whop, 2024; Empower, 2023).

Forget that casual Netflix binge; these are the invisible costs that shape every paycheck before rent or groceries hit.

Starting Line in the Red: College Debt as Entry Fee

But let’s not blame technology. Too many generational writers use social media and mobile phones as a crutch when describing why younger generations are so plagued with labels like entitlement or anxiety. The Millennial budgeting approach was shaped by far more than just technological advances.

Enter the heavy baggage of higher education. As of March 2024, Millennials (ages 28–43) held average student loan balances of $40,438, significantly more than any other generation except Gen X and higher than Boomers did at the same age (Experian, 2024). And let’s play this out. This is $40,438, not when they graduated, but today. Consider this, most Millennials have been out of school between six to 21 years and at this moment in time, still have that much debt. That right there would average about $300 - $400 a month in loan payments.

This isn't just numbers; this is a defining reality of approximately 3.87 million Millennials who carry these loans, carrying a weight that shapes every financial choice they make (Bankrate, 2023). They didn’t choose to be burdened—they were raised into debt by well-meaning parents who urged college at all costs.

Driving Beyond Education and Technology

This is not a woe-are-Millennials piece and how expensive their desired lifestyle appears to be. Instead, it shows just how profound an impact decisions made by parents have on an entire generation, and more so, how those actions made by parents impact a generation of people in the workforce.

Let’s continue. In 1997, as the first wave of Millennials turned sixteen, about 40% of 16-year-olds had primary access to a vehicle, and nearly 46% were licensed to drive (Federal Highway Administration [FHWA], 2001; Generational Driving Trends, 2024). Equally significant, but by this point not surprising, one-third (33%) of Millennials reported receiving their first car as a gift, a monumental jump from previous generations who did not have that same luxurious handout (Generational Driving Trends, 2024).

And here’s the kicker: only 12% of Millennials paid for their own car insurance before age 18. Insurance, like the car itself, was often tucked quietly into a parent’s budget. Freedom came prepackaged.

In practical terms, they weren’t just getting cars, they were being taught that mobility was essential, free, and frictionless. Their average daily trips hovered around 3.5 per day, largely by automobile and spanning 10–12 miles per trip, much of it for school, work, and social activities (NHTS, 2017; Generational Driving Trends, 2024).

We’ve since seen a sharp decline in early licensure and vehicle access with Gen Z, but that’s a conversation for another time. The point here is this: Millennials came of age with keys in hand, gas in the tank, and no monthly payments to make.

And yet, when they graduated into adulthood, that baseline didn’t vanish. It just got more expensive. Once the keys were handed over, financing, insurance, gas, and upkeep became non-negotiable financial items in any grown-up budget.

Leaders: Hear the Signals, Then Ask Why

There was a season, primarily in the mid-2010s, when Millennial employees seemed to be constantly asking for raises. For many leaders, particularly Gen X and especially Boomers, it triggered a quiet frustration: Why do they feel so entitled? Why isn’t their salary “enough”?

But here’s the missing piece: Millennials weren’t just asking for more because they wanted more. They were asking because they needed more. Or at least felt that they did.

Raised in a world where internet access, smartphones, car insurance, and monthly subscriptions weren’t optional but expected (often provided by parents), they entered adulthood carrying a lifestyle they hadn’t yet earned. Add student loans on top, and what used to be discretionary became essential. They were budgeting from the bottom up, starting with fixed costs and working backwards toward survival. That raise request? It wasn’t indulgence. It was math.

Too often, leaders still miss the deeper “why” behind a financial ask. Instead of rolling their eyes at another compensation conversation, pegging the requestor as entitled, the better question is: What assumptions shaped this employee’s financial reality? That shift from frustration to curiosity is where true leadership lives.

This doesn’t mean organizations need to shower employees with raises or build policy around entitlement. In fact, it may mean something far simpler: offering budgeting resources, financial literacy courses, or even just listening differently. It means recognizing that Millennials weren’t just spoiled, they were set up.

And ironically, it was often those same leaders who get so flustered by the seeming sense of entitlement that did the “setting up” of the generation.

A Generational Echo and a Subtle Reckoning

Boomer (and some Gen X) parents gave their Millennial kids everything they never had. The car at sixteen. The cell phone in high school or even middle school. The college degree, no matter the cost. They paved the road with love and ambition but never explained how long it took to afford the pavement.

Millennials didn’t mistake luxuries for entitlements. They were taught those were normal. Then, right as “normal” got more expensive, streaming, devices, connectivity, insurance, loan repayments, they were released from the nest and expected to self-sustain. It was a perfect storm: rising essential costs paired with rising expectations, handed down without instruction.

Understanding that story doesn’t justify every raise request. But it does reframe the narrative and invite leaders to close a gap not with policy, but with perspective.

What Comes Next - Thoughts on Gen Alpha

If Millennials were budgeting out of survival, Gen Alpha may chart an entirely new course. Many Millennials are now shifting away from materialism in how they raise their children, opting for experiences over gadgets. Less “give them everything,” more “teach them how to value it” or “give them an experience they can remember and that will last.”

Gen Alpha might be the most well-traveled, tech-integrated generation in history, but they may also grow up with a clearer view of what truly matters. Not because the world gave them less, but because Millennials learned, slowly, how much it costs to give too much too soon.

And that, too, is a leadership insight. Because what you model—financially, emotionally, and culturally has staying power. Budgeting is no longer just personal finance. It’s a legacy.

Generational Snapshot

Thank you for reading!

Until next time,

Works Cited

Bankrate. (2023, September 27). Survey: Most student loan borrowers are making sacrifices to afford payments. https://www.bankrate.com/loans/student-loans/student-loan-debt-statistics/

Empower. (2023, August 16). The one thing Millennials want in 2024: Subscriptions. https://www.empower.com/the-currency/money/one-thing-2024-august-16

Experian. (2024, March). State of student loan debt in 2024. https://www.experian.com/blogs/ask-experian/state-of-student-loan-debt/

Federal Highway Administration. (2001). Highway statistics summary to 1995: Driver licensing. https://www.fhwa.dot.gov/ohim/summary95/dl200.htm

Generational Driving Trends. (2024). Teens aren’t driving like they used to. GenerationTech Blog. https://www.generationtechblog.com/p/teens-arent-getting-their-drivers

National Household Travel Survey [NHTS]. (2017). Daily travel quick facts. U.S. Department of Transportation. https://nhts.ornl.gov/quickfacts

Pew Research Center. (2019). Millennials and technology: Then and now. https://www.pewresearch.org/short-reads/2019/09/09/us-generations-technology-use/

Savanta. (2024, March 6). Gen Z and Millennials shaping the subscription economy. https://savanta.com/knowledge-centre/view/gen-z-and-millennials-shaping-the-subscription-economy/

Whop. (2024, January 12). Subscription statistics for 2024: The true cost of convenience. https://whop.com/blog/subscription-statistics/

Reply